Ever since Walter Morgan created the balanced fund in 1929, the “60/40” model has been the dominant approach to portfolio allocation. However, this may be about to change: in the wake of the longest equities bull market and a nearly 40-year trend of falling interest rates, the 60/40 may have reached its limits. With many stocks trading near all-time highs and yields near all-time lows, even a modest rise in interest rates could result in negative returns.

These conditions led many analysts to sound alarm about the risks of traditional 60/40 approach. The emerging view, expressed in a recent Bank of America report, “The End of 60/40” is that, “The future of asset allocation may look radically different from the recent past, and it is time to start planning for what comes after the end of 60/40.” Indeed, effective asset allocation will require nimbler, more tactical approaches backed with high quality decision support technologies.

To meet this challenge in a sustainable way and at scale, we can propose different versions of Dynamic Portfolio Allocation, an all-weather asset allocation process managed in real time with I-System Trend Following. Thanks to the I-System we can offer better and more consistent performance for the long haul, without depending on costly analysts and advisors. This will facilitate a significant reduction of costs associated with management and research. In addition, the process is fully transparent and free of conflicts of interest.

Example 1: Altana Systematic Portfolio Allocation (ASPA)

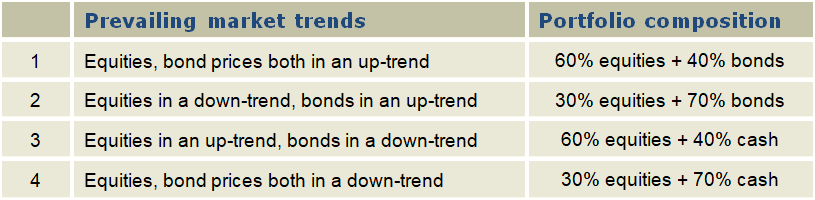

Last year we’ve developed a Dynamic Portfolio Allocation product for London and Monaco based asset manager Altana Wealth. ASPA uses I-System trend following in conjunction with a simple set of rules that dynamically adjusts the portfolio mix between stocks, bonds and cash according to the prevailing market trends:

We can use I-System strategies to determine the portfolio mix between stocks, bonds and cash according to prevailing market trends. The allocations can be dynamically adjusted using a simple set of rules as the following example:

We compared the performance of a traditional 60/40 portfolio vs. the trend-driven systematic portfolio allocation process using the S&P 500 as a proxy for equities segment and US 10-yr T-Note as proxy for the bonds segment. The comparison is illustrated in the chart and the table on the next page:

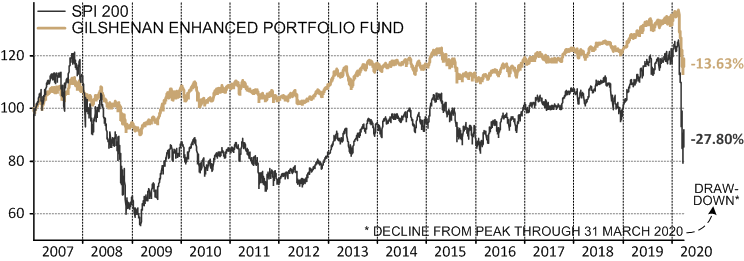

Example 2: Gilshenan Enhanced Portfolio Fund

We developed a similar product for the Australian asset manager, Gilshenan Capital, again with significant improvements over the traditional 60/40 approach, particularly through severe market corrections as we saw in March 2020:

Example 3: Dynamic Allocation With Tail Risk

A variant of the “60/40” portfolio – whether with dynamic trend-based portfolio adjustments or without – can also include a tail-risk component using I-System Trend Following to hedge both stocks and bonds exposure, but also include some exposure to alternatives like energy, metals and agricultural commodities.

Using I-System Trend Following, we can offer robust, sustainable solutions at scale and achieve superior and more consistent performance. Our partners like Altana Wealth and Gilshenan Capital are able to manage all market exposure with I-System Trend Following with no need for other forms of research or human expertise, enabling them to offer competitive products and compelling value to their investors.