Inflation: the #1 risk for investors

Inflation is the single greatest macroeconomic risk facing investors. Since 1960, more than two thirds of the world’s market economies experienced episodes of high inflation. On average, investors lost 53% of purchasing power during such episodes.[1] In many cases losses of wealth were significantly higher.

Managed futures: the most effective antidote

Empirical evidence has shown that exposure to commodity futures represents far and away the best hedge against inflation. For example, in the paper titled, “Assessing Managed Futures as an Inflation Hedge Within a Multi-Asset Framework,” published in the Journal of Wealth Management (April 2011), the authors concluded that, “Managed futures outperform the other asset classes… No other asset class presents itself as a viable inflation hedge.”

Their finding corroborated an earlier Alliance Bernstein’s research which found that “managed futures” (i.e. exposure to commodity futures prices) had the highest inflation beta of all asset classes:

This could particularly be valid at present: relative to equities, commodity prices have declined to 50-years lows in 2020, and remain relatively low in spite of a partial recovery during 2021 and 2022.

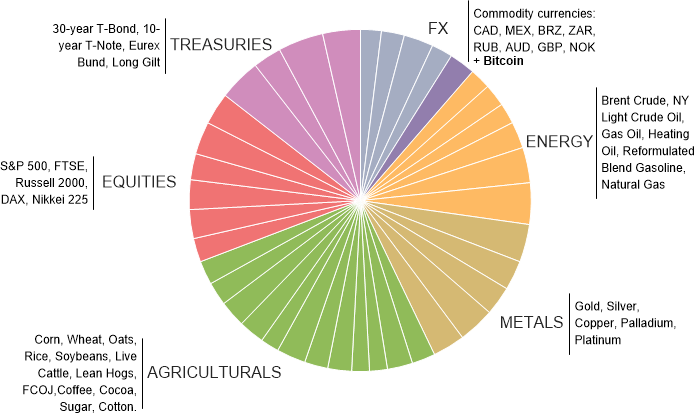

The looming commodities super-cycle

The industry now faces an acute shortage of portfolio diversifiers at a time when it must take ever more risk to achieve its return targets.

Eric Peters, CIO, One River Asset management

A mere reversion toward that norm may present not only an inflation hedging effect, but also an attractive investment opportunity in its own right as well as a valuable, real means of diversification just when this is most needed. This reversion, expected to span the next ten to 25 years, has begun in 2021 and adding exposure to commodities like energy, metals and key agricultural crops in a well-diversified portfolio could be among the most compelling investment alternatives for the decade of 2020s.

To read a simple explanation of the 3-step process of constructing this type of a portfolio, please consult the following PDF document.

We’ve done this before and outperformed world’s leading, Blue Chip managed futures funds!

The portfolio management process we propose is effective and supremely reliable, offering a low-cost alternative to costly in-house management and research teams. Managing broadly diversified portfolios across 50 or more futures markets is exactly what the I-System was built for and where our audited track record stood out, head-and-shoulders above most of our peers.

From 2007 to 2013 we managed under Galstar Derivatives Trading and the stellar track record we achieved is a live (and audited) testimony to the quality and reliability with which we can offer this service.

This result was not a lucky fluke: it was based on trading in 39 financial and commodities markets using 120 I-System strategies and about 10,000 individual trades. The results are also repeatable, given that they were entirely based on a set of precisely defined and thoroughly tested rules defining exactly which risks were taken, how much risk and how that risk was managed.

For further information about our Inflation Hedging portfolio solutions please consult the PDF brochure at the link above, which shows how we construct a managed futures portfolio. For additional details you may contact us by writing to TrendCompass@ISystem-TF.com

Notes:

[1] Stanley Fischer, “Modern Hyper- and High Inflations,” National Bureau of Economic Research Working Paper No. 8930