At market close on 15 December, the Tesla’s market cap ($606.5 billion) surpassed that of Toyota, General Motors, Daimler, VolksWagen, BMW, Honda and Ford combined ($578.2 billion)! This underscores yet again the power of market trends and the momentum investing strategy. Let’s have a brief look at the way this shaped up.

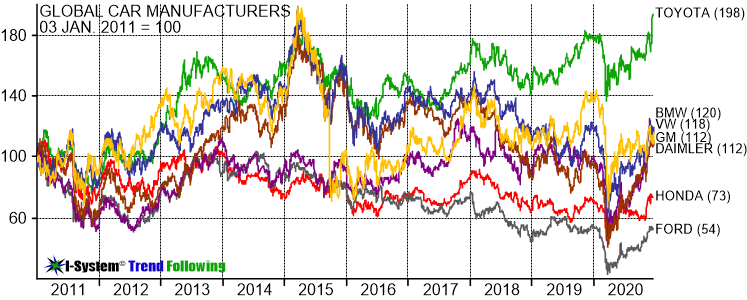

While the S&P 500 appreciated by almost 300% over the last ten years, car manufacturers haven’t been a great investment. For every dollar invested in Toyota, you’d have about two today. If you were unlucky to invest in Ford Motor Co, your investment would be worth just over half. With most of the others, you’d be about even. Then there’s Tesla… Here’s the picture, on logarithmic scale (else other manufacturers’ stock prices look like a bumpy flat line):

Although Tesla’s valuation would be hard to justify on any rational basis, the undeniable reality before us is that Tesla has massively outperformed its peers – a trend that’s held throughout the past decade. If you had the wisdom and the foresight to invest in Tesla and hold it for ten years, you would have done extremely well: between July 2010 and October 2021, Tesla’s shares appreciated 387-fold – a compound annualized rate of return of almost 72%. But who has such wisdom and foresight? Probably not very many people. However, if you sought to systematically pick the best performing stocks and invest in them regardless of what you thought about the companies in question, their valuation, products or their management teams – there you’d be on to something… This is what’s called momentum investing.

The power of momentum investing: empirical evidence

Tesla’s ascent was not an anomaly but only a fresh, if spectacular, case of the recurring theme: that markets move in trends. When trends get going in earnest, they often eclipse all our notions about rational asset valuation, both on the upside and on the downside: think of things like Bitcoin and Palladium or stocks like Amazon, Microsoft, Facebook, Tencent and others. Momentum investing, a variant of trend following, seeks to systematically pick such ascendant stocks and hold them for as long as they outperform. How well does this strategy perform? It performs remarkably well.

A very extensive empirical study covering over a century of data showed just how well momentum investing performs. London Business School researchers Elroy Dimson, Paul Marsh and Mike Staunton analyzed stock market price history starting from 1900. They constructed investment portfolios by selecting 20 top performing stocks in the previous 12 months from among UK’s 100 largest publicly trading firms, and compared their performance to portfolios of 20 worst performers, re-calculating the portfolios every month.

They found that lowest-performing stocks would have turned £1 invested in 1900 into £49 by 2009. By contrast, the top performers would have turned £1 into £2.3 million,[1] a 10.3% difference in compound annual rate of return.

The gap between investments in best and worst performing stocks was even wider when data from the entire London stock market was taken into account. From 1955 onward, the top performers generated an 18.3% compound annual rate of return vs. 6.8% return for the laggard stocks. Dimson, Marsh and Staunton found that the strategy was “striking and remarkably persistent” as it proved successful in 17 out of 18 global markets studied with data going back to 1926 for America and to 1975 for larger European markets. The only exception was Japan, where the results were based on post-2000 data.[2]

The significance of the Dimson, Marsh and Staunton study is that it has provided some of the most compelling evidence for the case that market trends represent the most potent driver of investment performance over the long term.

The trend follower’s and momentum investor’s advantage is that he does not need to exert himself intellectually to determine the right valuations at which to buy or sell assets. Loud and clear, the markets themselves communicate to us which assets are in favor and which in disfavor. For many investors this may seem too simplistic, but the evidence supporting this approach is extensive and robust. Even Warren Buffett and Benjamin Graham, the very icons of value investing owe their outperformance to momentum investing rather than superior value picks. If you are sceptical of this claim, I trust you’ll find my analysis hard to refute: Why Trend Following Beats Value Investing.

The above is a partial excerpt from my book “Mastering Uncertainty in Commodities Trading”

Momentum investing portfolios are one of the turn-key portfolio solutions we propose to asset management organizations – for more information, please see here.

Notes:

[1] These figures correspond to the outcome at the end of 2009, following the 2008 market crash. At the close of 2007, the figures were even more impressive: the portfolio of winners generated a compound annual rate of return of 15.2%, turning £1 invested in 1900 into more than £4.2 million. The portfolio of worst performers would have returned only 4.5% a year, turning £1 into £111.

[2] Financial Times, “Momentum effect gains new admirers” by Steve Johnson, 23 January 2011- http://www.ft.com/cms/s/0/8d7c8a92-26c6-11e0-80d7-00144feab49a.html#ixzz1I0Zl0FZP