On August 15, 2021 when the Taliban took over Kabul, I posted an analysis in which I noted that the event would prove to have very far-reaching consequences and that it would be the United Kingdom which might sustain the greatest setback from it (a 14-min video report is here). This was confirmed by an avalanche of furious reactions and unanimous condemnations from London. For example, in a London Times article, Foreign Secretary Dominic Raab denounced the American isolationism: “America has just signaled to the world that they are not that keen on playing a global role. The implications of that are absolutely huge. … We are going to have to do a hard-nosed revisit on all our assumptions and policies.” The gravity of the event from the British perspective was perhaps best captured in a single sentence uttered by none other than UK’s former PM Tony Blair. In an interview with Sky News on 23rd August he said, “we are at risk of relegation to the second division of global powers.”

Empire in turmoil

Reactions and contingency plans were considered with some urgency in the British halls of power. DailyMail dramatically announced that “Across Whitehall and in British embassies around the world, officials and diplomats are adjusting to the fact that Mr. Biden has adopted an America First policy every bit as isolationist as his predecessor’s.” While many people think of today’s Empire as the American empire, my contention has been that it is in fact a vestige of the British Empire with stakeholders in several nations, principally the UK and USA. The UK has now rebranded its leadership as “Global Britain.”

The “special relationship” between the US and Britain has been something like the Master-Blaster combination. For those old enough to remember the film Mad Max 3, Master is an old, decrepit dwarf propped up on the back of the “Blaster,” a powerful, muscular giant. The Master manipulates Blaster to fight his fights and subdue his enemies. But ultimately the combat-fatigued Blaster is defeated, ending the Master’s supremacy. This metaphor could well be fitting of today’s geopolitics.

End of the road?

For over three centuries, the UK has enjoyed disproportionate influence in the world as a naval superpower and an empire. Even in the 20th century it has remained one of the world’s leading political, diplomatic and military powers. It has enjoyed a close alliance with the US and has continued to wield decisive influence over many of its former colonies. London has also shared with New York the primacy as the world’s financial capital and headquarters of many of the most powerful multinational corporations and banks.

But today Global Britain faces gathering head-winds. Its special relationship with the US is no longer as reliable as it has been over the past 100 years and it could still deteriorate further. With Brexit, it has lost influence in the European Union. Its recent policy of strengthening trade and financial ties with China, still earnestly implemented by the David Cameron and George Osbourne cabinet has entirely ground to a halt, bringing Chinese investment in the UK to near zero.

Britain’s most recent accession to the AUKUS military alliance with the US and Australia has set the UK on the path of possible military confrontation with China. In the process, it has also alienated France. In addition to all that, Britain could soon be facing another crisis in the Atlantic. Namely, Argentina’s recent deal to purchase military equipment from Pakistan – the deal that Britain successfully blocked only last year, could soon jeopardize its control of the Falkland Islands. If there’s been any good news for Global Britain, I am not aware of them at this time.

Asia is the prize

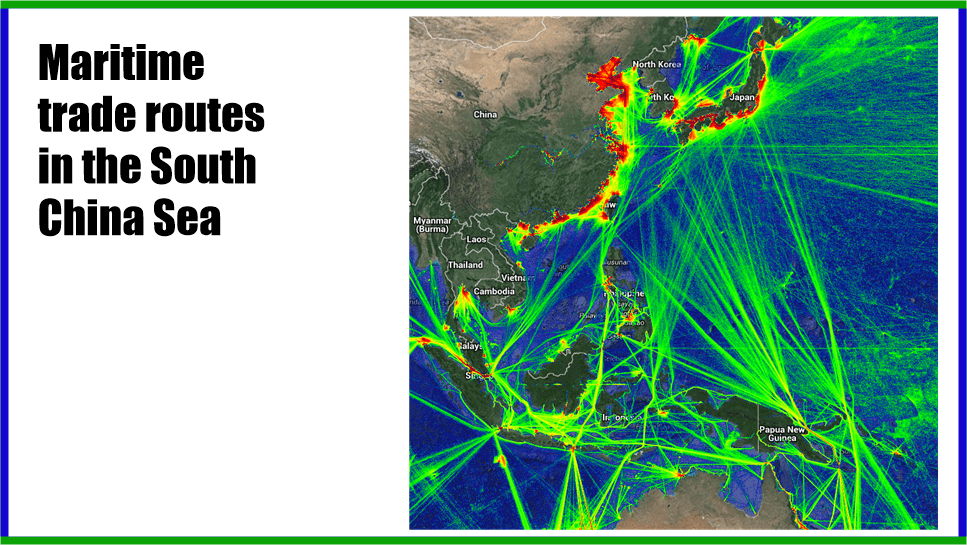

None of this diminished the British establishment’s desire in to defend its imperial ambitions. Having thrown off the restraints of its EU membership, Britain has turned its focus on the Indo-Pacific region, presently sailing its Royal Navy fleet around South China Sea, touring the area’s 40 nations and conducting war games with allies like South Korea and Singapore. The objective of this show of force was well articulated by the flotilla’s commander, Vice Admiral Jerry Kyd: “This is the part of the world where… the navy has retreated in the past 20 years but recent review has made it quite clear, we want to have a more persistent and enduring presence here…”

The Vice Admiral explained why they want to be present in the region half way around the world from home: “One third of world trade flows through South China Sea… so it is natural that the United Kingdom wants to have a presence…” But in the age of hypersonic precision-guided missiles, the 18th and 19th century gunboat diplomacy won’t impress Asia’s emerging powers, let alone Russia or China. As multiple simulations of conflict in the Pacific showed, even in alliance with the US, Australia, and Japan, the empire would be unable to defeat China. Thus, while Global Britain’s imperial ambition to once more rule the waves will certainly come at a high cost, it is unlikely to pay off in terms of treasure.

Britain’s deteriorating fiscal position

All of these developments have accelerated while the Kingdom’s economic and fiscal position is rapidly deteriorating. During the decade from 2010 through 2019, British economic growth averaged a very sluggish 1.83%. But with last year’s pandemic it collapsed by almost 10% in 2020. In response to the pandemic, the government added £407 billion in expenses and £355 billion in new debt, which is on track to reaching £2.8 trillion in 2025, or about 110% of the GDP. The magnitude of these figures is easier to appreciate in per capita terms: we are talking about almost £47 thousand per man, woman and child in Britain and over £100 thousand per household. Again, many learned economists will try to convince you that debts and deficits don’t matter because the interest rates are so low that the government can simply issue gilts as required and raise unlimited debt for free.

Of course, these are hollow reassurances: the world does not have infinite appetite for British debt and the interest rates may not remain low forever. At the beginning of 2021 interest rates on the gilts was 0.5%. Today they have doubled to over 1%. This change alone has added about £10 billion in interest expense on government debt. Every 1% increase will add further £20 billion to government deficits, well over £700 per household. Britain’s government will have to significantly increase taxes and this year, the Boris Johnson cabinet has already announced significant tax increases on households and corporations. The planned changes will bring the government’s tax receipts to about 35% of the GDP, the highest level in over 50 years.

Broadly speaking, nations have two alternative ways to deal with the problem of high debts: either they can seek to increase their wealth or they can default through outright repudiation, currency devaluation or through inflation. Today, it is highly unlikely that the UK can increase its wealth enough to substantially reduce its debt burdens. The financial repression and savage austerity at home will probably suffocate domestic economic growth.

Increasing wealth through colonial conquest is also unlikely to succeed. All the same, Britain won’t revert to simply minding its own domestic affairs as a neutral island nation, and will endeavor to regain its lost hegemony to the bitter end. As the American economist John Kenneth Galbraith said, “People of privilege will always risk their complete destruction rather than surrender any material part of their advantage. Intellectual myopia, often called stupidity, is no doubt a reason. But the privileged also feel that their privileges, however egregious they may seem to others, are a solemn, basic, God-given right.” This all sets the UK on a predictable downward spiral typical of history’s declining powers.

The market view

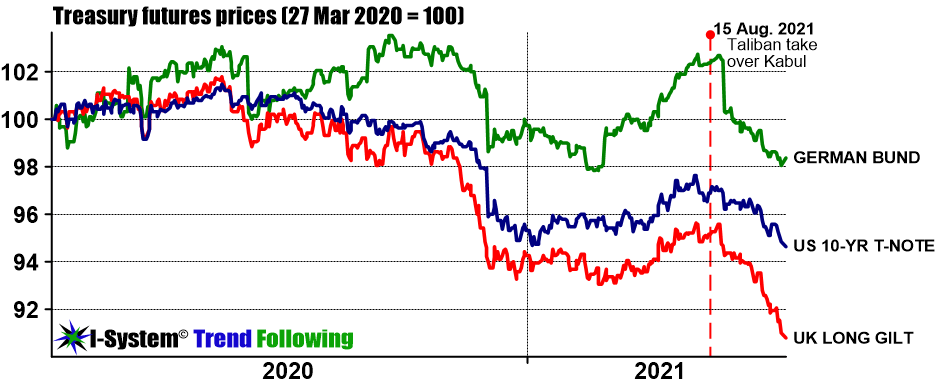

Leaving the complexities of economics and geopolitics aside, let’s have a glance at how the markets have been reacting to the changing circumstances. Only days after the Taliban took Kabul the prices of western nations’ Treasury bonds began to decline sharply. But among the major powers, it was the British debt that has been losing ground most rapidly. The chart below shows the comparative performance of the UK, US and German treasury bonds:

I thought it would be interesting to see these changes starting from 27 March 2020, the date that coincides with the passage of the CARES Act in US Congress. That date marks the stealth banking coup in the West and the beginning of the rapid deterioration of all three nations’ fiscal positions.

If we are to give credence to the Wisdom of the Crowd hypothesis, the divergence between the German, US and UK treasuries are not random and the markets have clearly soured the most on the UK and singled it out as the weakest player (in addition to its sidekicks, Canada and Australia). I believe that over the medium- to long-term, this trend will probably persist and gather momentum.

How bad could this get?

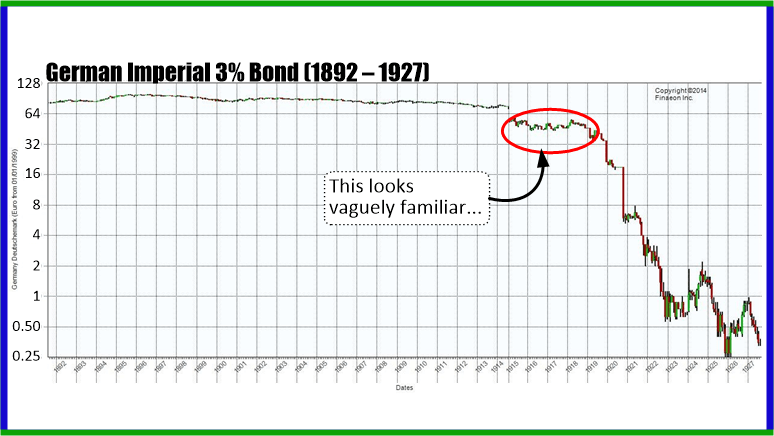

Our next question is, how bad could it get? Certainly, a substantial increase in interest rates and further decline in treasury prices are all but certain. A few years ago I came across the chart of the German imperial bond between 1892 and 1927. I think we should not draw any definitive conclusions from what happened in Germany one hundred years ago, but this shows the extreme consequences of the financial and economic imbalances plaguing a fallen empire.

To be sure, the above chart was drawn on logarithmic scale and the collapse phase only becomes clear after 1919. However, the pattern I circled does look interesting and similar to what we are observing today: a consolidation, an abortive up-trend in 1917/18, followed by a sharp collapse in early 1919 that only accelerated from there. On a linear scale, we could better discern that the trend reversal and slow, gradual decline spanned many years, beginning at the turn of the 20th century. It is important to appreciate that this collapse was not a foregone conclusion until very late in this cycle. German economy even recorded a remarkable boom period in 1920 and 1921. In his brilliant book, “Dying of Money,” Jens O. Parsson conveyed the mood of the moment based on the testimonies of economists and authors who lived through the period. Here’s what he wrote:

“Industry and business were going at fever pitch. Exports were thriving… Hordes of tourists came from abroad. Many great fortunes sprang up overnight. Berlin was one of the brightest capitals in the world in those days. Great mansions of the new rich grew like mushrooms in the suburbs. The cities… had an aimless and wanton youth and a cabaret life of an unprecedented splendor, dissolution, and unreality. Prodigality marked the affairs of both the government and the private citizen.” Unemployment was virtually non-existent and profitable speculation in the stock markets became one of the nation’s foremost obsessions. “The volumes of turnover in securities on the Berlin Bourse became so high that the financial industry could not keep up with the paperwork, even with greatly swollen staffs of back-office employees, and the Bourse was obliged to close several days a week to work off the backlog.”

Part of the pundit class of the day argued that deficits didn’t’ matter and that inflation wouldn’t escalate out of control because it seemed tame at the time. Writes Parsson: “Until 1922 and the very brink of the collapse, Germans and especially foreign investors were absorbing marks in huge quantities. Only the international reputation of the Reichsmark, the faith that an economic giant like Germany could not fail, made this possible. … investor’s willingness to save marks kept the marks from being dumped immediately into the markets, and thereby for a long while held prices in check. The precise moment when the inflation turned upward toward the vertical climb was undoubtedly timed by no event but by the dawning psychological awareness of the German and foreign investor that Germany was not going to back its money. With that, the rush to get out of the mark was on. Like a dam bursting, the seas of marks flooded into the markets and drove prices beyond all bounds.”

Today the UK could be in the early stages of the same sequence of events: a severe crisis at home coupled with the dramatic loss of international leverage and a very costly addiction to imperial prestige. The UK will likely make all the mistakes made by other powers in that similar positions through history: it will suffocate its domestic economic growth by imposing hard austerity at home while at the same time increasing military spending and foreign adventurism. Britain’s public debt will continue to outpace its GDP growth and the government’s budget deficits will be covered by Bank of England’s monetary inflation. This recipe reliably leads to stagflation and possibly to hyperinflation.

The likely outcome in the markets: FTSE up, bonds, pound down.

Predicting things is a thankless task but I do believe that, at a macro level, we can expect the following developments over the coming months and years: asset prices will probably continue to rise (i.e. a bullish cycle for the FTSE 100), but the government bonds will continue to slide along with the British pound.

How to navigate the changes?

While nobody can predict the timing or magnitude of these events, one thing we know is that large-scale price events (LSPEs) invariably unfold as trends and these can span many months and even years. The most reliable way to navigate the coming changes will be through high quality trend following strategies, precisely the kind of decision support we offer through I-System TrendCompass reports.

TrendCompass delivers reliable daily trend following signals on more than 200 different financial and commodities markets with monthly subscriptions starting from 100 Euros. Today I am considering putting together a report focused on the UK. It will cover the main UK markets like the FTSE 100, long gilt and the British pound vs. the US dollar, Euro and possibly some other currencies.

The subscription rates for the TrendCompass start at 100 Eur/month and I intend to price the UK-focused report at that level. If this could be of interest please drop me a note in the comments or write us by email: TrendCompass@ISystem-TF.com. One month’s test-drive is always offered free of charge and if you then decide this is not for you, there’s no further risk or commitment on your part.

For more information about the I-System and about the TrendCompass reports please visit ISystem-TF.com.

Books – now free thanks to Amazon.

Please note, further to a months’ long back-and-forth with Amazon.com over unpaid royalties, the abusive behemoth – literally hours after they’d conceeded that they owed me money – took the step of entirely deleting my account, books, reviews and all other records. With that they appropriated all the royalties owed. I can therefore not link any of my books, but if you are interested in reading them, please drop me a note in the comments and I’ll forward you a PDF copy free of charge. The titles are below:

Hi Alex. I got here because I follow you in twitter and I am also a trend follower . Thank you in advance for the pdf copy of your two books please kindly send to my email .

LikeLike

Hi Alex I forgot to write my email . here is my email dionisiobathan@gmail.com please kindly send here the books. Thanks in advanced.

LikeLike

Hello Alex,

How are you?

Thank you for sharing your insights. I am new to trading and your work and would be so grateful to read your books. Would it be possible to get copies of both books?

Thank you so much and I look forward to your articles.

Best

Jonah David

LikeLike

Hi Jonah, thank you – I’ll send the books but I’d need your email address.

Kind regards,

A.

LikeLike

Hello Alex,

Thank you for getting back to me. My email address is tcosylc@protonmail.com

Thank you so much and I look forward to reading your books.

Best

Jonah David

LikeLike

Hi Alex, I got here via your blog. I’ve been enjoying your geopolitical posts recently and I’d really like to read your trading books. Please could you forward me a copy of each? Many thanks!

LikeLike

Hello May, you’ll find links to download both titles under the “About” tab here.

LikeLike