Over the last few months many markets, including equity indices, treasuries, energy and other commodities have been in a holding pattern, either drifting horizontally or staging rallies, then reversing direction. These conditions make it hard for investors to earn decent returns, but they can be particularly frustrating for trend followers, resulting in drawdowns. A few months of drawdowns often suffice to lead some investors to bail or declare that a strategy is failing. However, drawdowns should be expected – they invariably follow a period of positive performance and investors who are too quick to react to them may do so at their detriment.

Unfortunately, most investors tend to underperform market benchmarks, which is almost entirely due to their tendency to chase after returns. Even the most celebrated “market wizards” aren’t immune to this fault. One of the most spectacular examples of this was when in the year 2000, Stanley Druckenmiller ploughed $6 billion of George Soros’ Quantum fund into tech stocks literally hours before the Nasdaq peaked and sustained a 50% loss in only six weeks. I detailed this fascinating story and Druckenmiller’s own account of it in my October 2020 article, “How Stanley Druckenmiller Missed Market Top by an Hour and Lost Half His Fund.”

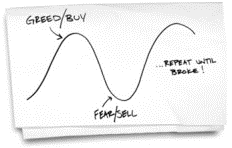

In the 2008 Journal of Pension Benefits, N. Scott Pritchard documented that from 1988 through 2007, while the S&P 500 returned 11.81% annually, the average investor achieved a return of only 4.48% [1]. In his commentary to Benjamin Graham’s “Intelligent Investor,” Jason Zweig suggested that investors achieve these results “simply by buying high and selling low.” Or as one blogger illustrated it succinctly enough:

Professional asset managers are equally susceptible to this error. In his 2010 report “Untangling Skill and Luck,” Legg Mason’s Michael Mauboussin cites a study by finance professors Amit Goyal and Simil Wahal, who studied how well 3,400 plan sponsors (retirement plans, endowments, foundations) performed at hiring and firing investment managers over a 10-year period. They found that plan sponsors hired investment managers after they had generated superior returns, only to see post-hiring returns revert to zero. They fired investment managers for a variety of reasons (poor performance topped the list), only to see the managers they fired deliver statistically significant excess returns. The key reason investors did worse than the average fund: they put the money in when markets/funds were doing well and pulled the money out when they were doing poorly.

It is not difficult to divine how and why asset allocators reach decisions that result in underperformance. An asset (or an investment product) at peak performance looks attractive with even a good looking set of statistics to show. By contrast, a decline in performance will make the statistics look much less attractive. But the key thing that statistics may not convey is the quality of the product: is it based on a valid investment strategy and is the investment process credible, well thought-out, and robust?

As Mauboussin concludes, “in evaluating an analyst or portfolio manager, it is much less important to see how she has done recently than it is to assess the process by which she did her job… And make no mistake about it: the reason to emphasize process is that a good process provides the best chance for agreeable long-term outcomes.”

In other words, qualitative analysis of an asset manager’s investment process might hold the key to improving investor performance: namely, basing their decisions on a deep understanding of an investment strategy and the management process in pursuit of that strategy. That understanding could avert the fear which induces investors to part with good investment after a period of drawdowns. It could also make them a better judge of when to sell a stellar looking investment. Investing involves periodically sailing through rough weather. In such circumstances, “keep calm and carry on,” is often the best approach.

[1] Pritchard, N. Scott. “The Tyranny of Choice – Why 401(k) Plans Are Failing and The Cure to Save Them.” Journal of Pension Benefits, Volume 16, Number 1 – Aspen Publishers, Autumn 2008.