(Originally written in November 2019) Back when I traded stocks in late 1990s, I had a gnawing suspicion that beyond the nonstop noise of the news flow, there was some force pushing the rising tide, but I couldn’t discern what it was. By today I think I worked it out. The most surprising thing about it is that it’s been so hard to work out.

Stocks are principally driven by money supply

The first time I encountered an explicitly formulated hypothesis that justified my suspicions was years later while I researched for my book, “Grand Deception.” The hypothesis, relating to Russian stocks, was articulated by Bill Browder, CEO of Hermitage Capital Management in his 2006 HedgeWeek interview:

“… Hermitage has identified a 90% correlation between money supply growth and the Russian RTS equities index from 2003 to 2005. Increases in money supply are highly correlated with an increase in equity values in Russia. Interestingly, the stock market has recently become more sensitive to changes in money supply then it was in the past. While the correlation has always been high (between 85% and 95%), the slope of the correlation line (i.e. the impact of new money on the market) has recently increased. For example, in 2004 there was a 1:1 relationship between money supply and the stock market (a 10% change in money supply would lead to a 10% change in the stock market). Now there appears to be nearly a 4:1 relationship. New money supply is having a much greater impact on the stock market.”

In other words, the predominant force behind the rise of Russian stocks was monetary inflation. Mind you, Browder was no ordinary hedge fund manager. He was – and still is – a well-connected operative in the way most investment managers aren’t. His partner in crime was Edmond Safra, the late owner of the infamous money laundering outfit, Republic National Bank of New York. After Safra’s mysterious death, his bank was absorbed by HSBC, which became Browder’s new and bigger partner in crime.

More recently Stanley Druckenmiller, another prominent money manager, articulated the same basic idea about what moves the stock markets:

“Earnings don’t move the overall market, it’s the Federal Reserve Board… focus on the central banks, and focus on the movement of liquidity… most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.”

Lost in the news flow…

While ordinary investors and market analysts exert themselves daily, analyzing a myriad of charts, business fundamentals, wholesale and retail sales, earnings reports, profit warnings, interest rates, employment and an endless alphabet soup of ratios and indicators, some investors understand the force that moves those great tides lifting all boats. Those investors can therefore make much larger, higher conviction bets, earn greater returns, and exit the scene before the tide goes out, stranding ordinary investors. When I read the Browder interview, I understood that he was almost certainly a western intelligence asset, that he worked for high-level financiers and was probably privy to higher level guidance. His statements to HedgeWeek corroborate this.

The empirical evidence

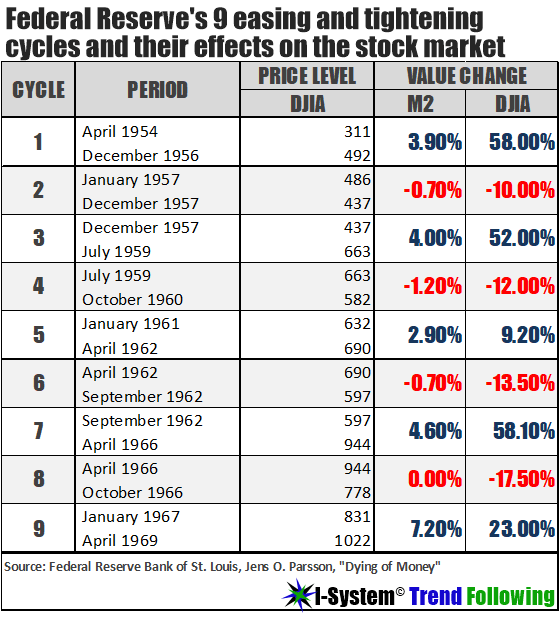

In his masterful 1974 book, Dying of Money, Jens O. Parsson provides further support for the above hypothesis:

“Monetary inflation invariably makes itself felt first in capital markets, most conspicuously as a stock market boom. … This happened at the commencement of the German inflationary boom of 1920, and it happened again at the commencement of the American inflationary boom from 1962 to 1966. Indeed, every monetary expansion in the United States since World War II was followed by a stock market rise, every cessation of monetary expansion by a stock market fall. Conversely, every stock market rise was preceded and accompanied by money inflation. Bull markets rest on nothing but inflation.” (See endnote [1])

Parsing through Parsson’s prose, ten such monetary easing and tightening cycles are covered (see table + paragraph below). And indeed, they almost perfectly coincide with great rallies and corrections in the stock market:

But what’s interesting here is not just the absolute expansion of money supply. If money supply contracts at all, it may lead to a stock market collapse. This was shown during the Nixon years. By 1969, monetary inflation expanded to almost 8% per year, the fastest rate since 1946. Then in May 1969 Federal Reserve began to tighten, reducing the money supply growth to 3.8%. Although this was still a relatively high rate of inflation, within two months, average stock prices dropped by 14% and within another year they were off by 31%!

The same principle was at work during and immediately after the roaring 20s (1930 through 1933). According to Murray Rothbard, “M” money supply was growing at an 8.1% annual clip from mid-1921 through 1928 fuelling a nearly 25% annual inflation of stock prices.[2] Today’s bull market is no different. In 2016, economist Brian Barnier of ValueBridge Advisors showed that the Fed’s Quantitative Easing (QE) program was behind 93% of the great 2009-2016 bull market.

Indeed, as Parsons wrote, “The stock market dances to an inaudible tune that is played for it by the government’s money inflation or deflation … A man who fully understood what inflation was doing at all times would seldom be surprised by the stock market. Armed with that understanding and little else, he could participate profitably in every stock market rise, step aside safely from every stock market fall, and shepherd his property with reasonable security through the bombardment of inflation or deflation. … When the government first turns on money inflation in times of slack business, the money has no work to do yet and nowhere to go but into investment markets. So the markets rise, even though business is still bad. … A rising stock market signals nothing but freshening money inflation. It is the earliest and most sensitive indicator of the inflationary train of events to come.”

So, what’s next?

Back in 2016, while ‘smart money’ was turning very bearish on stocks, I suggested that markets might not collapse and that instead, “we could see a significant and sustained rise in equity markets,” if central banks remain committed to supporting asset prices. Now we know. We also know that this commitment has not changed. The last abortive attempt at quantitative tightening in 2018 promptly triggered an almost 20% correction in the S&P500, but once the Fed reversed itself, so did the stock prices. The Fed can’t risk tightening anymore; keeping the bubble going is the only option, requiring an ever-expanding QE.

This may have sealed the endgame: an accelerating bull run accompanied by hyperinflation after which comes an epic crash. I pray that I’m wrong.

I originally posted this article on my blog, The Naked Hedgie in November 2019.

Alex Krainer is the founder of Krainer Analytics, creator of I-System Trend Following and commodities trader based in Monaco. He wrote the award winning book “Mastering Uncertainty in Commodities Trading” (best commodities trading book in 2021 and 2022).