After the 2008/9 financial crisis, managed futures funds emerged victorious from the rubble. As equity markets around the world collapsed and most hedge fund strategies sustained severe losses, the CTAs generated strong positive performance, because most of them rely on systematic trend following strategies, which means that they tend to perform well during bear markets.

What killed the CTAs

The multiple coordinated central bank QE programs artificially reflated many asset prices and caused heavy distortion of market signals. This in turn took a toll on most active investment strategies, as shown in this remarkable chart from Goldman Sachs:

In this environment, the CTAs fared no better:

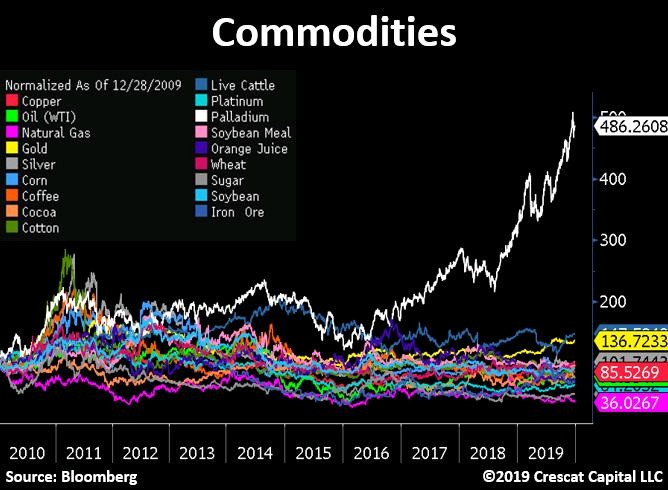

To be sure, market trends did not entirely vanish, but they were few and far between in the commodities markets:

As a result, already in 2014 the Financial Times reported that, “after years of poor performance,” 156 CTAs had gone out of business.[1] Since then, many more shut down, including some of the largest and most admired names among them. Not surprisingly, the media commentariat declared trend following dead and buried. But I believe that this view is mistaken and that trend following might soon experience a renaissance.

Why trend following is coming back

At present, global markets are beset by extremely precarious imbalances: monetary inflation has reached astronomical proportions; levels of debt and fiscal deficits in virtually all industrialized nations are unsustainable; interest rates are still near historical lows (in many markets still below zero) and stocks are at record high valuations.

The risk of a real bear market

On Friday, 02 April 2021 the S&P 500 broke 4,000 points for the first time. This should not have come as a surprise and I wrote about it repeatedly since October 2016 (that was back when “smart money” was being ultra-bearish). The reason this should have been clear was Federal Reserve’s commitment to supporting asset prices (see my article, “The One Force Moving Stock Prices…”). The only time this commitment came into question was during the 2nd half of 2018 when the Fed announced tapering of the QE and began to unwind its balance sheets. The result was a 20% crash in equity prices after which the Fed quickly reversed gear and reopened the monetary spigots. This episode made it clear that an ever accelerating QE was central banks’ only policy option. The result is a reflated asset bubble which is still with us.

Today it is impossible to predict just how high or for how long this bubble might inflate, but its ultimate fate is entirely predictable. Without exception, all asset bubbles ultimately burst and so will the present one. From that point on, the markets might tip into a real bear market: not a 2-3 year correction that we’d grown accustomed to since the 1980s, but perhaps something more akin to what we saw after the 1920s bubble burst:

or Japan’s 1980s bubble:

A real bear market can span more than a decade with equity prices retreating by 80% or more. In this environment systematic trend following might shine again. Trend followers do not bother about market valuations, don’t generally buy the dips, and don’t try to dig themselves out of a hole by averaging down. When their algorithms tell them to go short, they go short and stay short until the algorithms tell them to go long again. Here’s how ‘yours truly’ generated a +27% net return during the last bear market in 2008:

The commodities super-cycle

The commodities slump we touched upon already, created an anomalous imbalance between the prices of commodities relative to other asset classes.

What this chart shows is that central bank monetary inflation flowed largely toward equities (and other asset classes), but for some reason bypassed commodities. The anomaly looks more stark still from a 200-year perspective, showing a commodity price index alone:

The market pendulum is likely to swing back in the opposite direction, and unleash a cycle of major price readjustments – a widely anticipated commodity super-cycle. And while the timing and magnitude of such large price events tend to be entirely unpredictable, they will almost certainly unfold as trends and shape up over a number of years. When these trends begin to emerge in earnest, trend followers will likely regain their former glory. Recall, until the distortions brought on by QE, trend following was the most successful strategy of active investment management:

Indeed, market trends have been with us since the dawn of civilization. More than 2,000 years ago Sun Tzu wrote in “The Art of War” that there are three great avenues of opportunity: events, trends and conditions. In the 18th century Japan, trader Munehisa Honma took advantage market trends to build up a large fortune speculating on the Dojima rice market in Osaka during the Tokugawa Shogunate. Honma was credited with the invention of candlestick price charting and in 1755 wrote the book “The Fountain of Gold,” perhaps the first ever treatise on trading and market psychology. He described the ebb and flow of markets in trend moves: Yang bull markets and Yin bear markets.

The mindset barrier

In spite of the undeniable success of trend following strategies, most investors continue to regard trend following as an oddity, not entirely fit for the ranks of serious market professionals. The reason for this has nothing to do with performance but is in part simply cultural. Namely, most of today’s market professionals were educated in the Cartesian tradition which validates rigorous scientific method as a way to acquire knowledge. Value is placed on understanding linear cause-and-effect relationships that allow us to make predictions about stuff. This mindset has an obvious appeal in investment speculation: we expect to predict and profit from market events by understanding how the conditions we observe would cause them. That mindset also gives us the comfort in the sense of competence and control.

Trend following is a cultural misfit in this intellectual tradition. To begin with, it is based on a field of study called technical analysis where knowledge accrues through judgment heuristics and experience rather than empirical science. Trend following also blurs the relationship between intellectual work and its expected results. The linear thinking investor judges a transaction according to an explicit understanding of how and why that transaction should generate a profit. The trend follower simply implements a set of predefined rules, accepting that any given transaction may produce a loss. A trend follower expects profits, not from any particular transaction, but from a long sequence of trades extending far into the future.

Thus, while the conventional approaches to investing stem from an understanding of a particular situation, trend following is based on the belief that a certain predefined speculative behavior will deliver positive results over time, regardless of the economic situation, industry, market, or geography. Incidentally, this is another great advantage of trend following: if you learn how to read the charts, or formulate high quality trend following strategies, you’ll be able to greatly enhance your universe of opportunities. By understanding trends, you’ll be able to trade securities even if you don’t know everything about them. Over the last 20+ years, I’ve traded in well over 50 different financial and commodities futures markets and I can confess that I know next to nothing about most of them. I merely believe that they move in trends and that with a disciplined adherence to a well-formulated set of rules I’ll be able to capture profits from such trends as and when they emerge.

The above is a partial excerpt from my recent book, “Alex Krainer’s Trend Following Bible.” Amazon has removed it from its listing (along with the other two books I’d published) so it’s now available as a free download. You’ll find it on the “About” page of this website.

[1] Marriage, Madison: “Trend-following hedge funds’ future in doubt” – Financial Times, 07 September 2014. https://www.ft.com/content/c9b78c5a-350e-11e4-aa47-00144feabdc0