More than a century of empirical data covering 18 of the world’s largest stock markets show beyond a shadow of doubt that market trends are the most powerful drivers of investment performance.

The foundations of a successful long-term investment management practice should rest on four pillars:

- Truth

- Strategy

- Discipline

- Patience

Truth is what we try to uncover by observing the world around us, researching, analyzing and sharing knowledge. Strategy is what we try to formulate on the basis of what we learn about the world and the markets. On the back of my 25 years’ experience as a market analyst, researcher, trader and hedge fund manager I’ve come to a very firm conviction that trend following, and more specifically SYSTEMATIC trend following, is the most reliable strategy to achieve long-term success at investment speculation. That’s because markets move in trends and we can see this in all kinds of markets including stocks, bonds, currencies, commodities, and virtually any market where people trade.

Trends have been with us since the dawning of civilization and already two thousand years ago in his timeless classic, “The Art of War,” Sun Tzu named trends as one of the three great avenues of opportunity. Today it is enough to look at the price charts of various assets to identify trends beyond any shadow of doubt.

One of the most remarkable stocks of the last decade was that of the electric car manufacturer Tesla. Between July 2010 and October 2021, Tesla’s shares appreciated 387-fold, from just over $3 to $1,220 – a compound annualized rate of return of almost 72%. That appreciation had little to do with any fundamentals based valuation of Tesla’s shares, yet the trend endured for more than 11 years and that made it possible for investors to generate very substantial windfalls. Of course, such extreme price events defy all our notions of rationality and value, which makes them unpredictable.

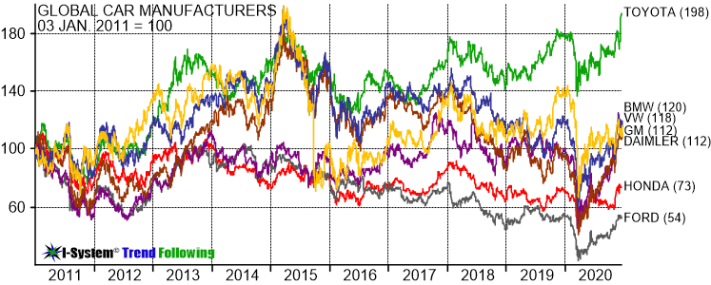

Tesla vs. other car manufacturers

Near the end of 2020, Tesla’s market cap surpassed that of the next seven large car manufacturers combined and in January 2021 it surpassed the total market cap of the next ten largest car manufacturers. Over the ten years’ interval from 2011 through 2020, the S&P 500 index increased by about 300%. However, the car manufacturers have not been a great investment during that time.

If you invested a dollar in the shares of Toyota in 2011, by the end of 2020 you’d have about two dollars. If you were unlucky to invest in Ford you’d have about half a dollar and with the others, you’d get something in between. All in all, nothing much to write home about. Here’s how that compared to Tesla:

I set the charts to a logarithmic scale because on a linear scale, the price charts of other car manufacturers look like just a bumpy horizontal line compared to Tesla’s stock price.

The significance of this case

Tesla’s stock price appreciation would be difficult to justify on any rational valuation basis, but if your objective is generating investment returns then this point is in fact irrelevant. The undeniable reality is that Tesla – for whatever reason – had massively outperformed its peers in a trend that’s held for over a decade. It is important to understand that this is not an anomaly but only a recent, if spectacular example of the recurring theme: that markets move in trends. And once trends get going in earnest, they regularly eclipse our ideas about asset valuation, both on the up-side and on the downside. This happens regularly: it is not an exception that should surprise us.

For anyone who had the foresight to buy some Tesla shares in twenty-eleven and the wisdom to hold them for ten years, they would have earned more than $120 for every dollar invested. However, not many of us have such foresight or wisdom – nobody could have predicted Tesla’s stock’s success over such a long time interval. But instead of trying to predict the unpredictable, what if you always just picked winners?

Momentum strategy: the empirical evidence

Suppose you systematically invested in top performing stocks, regardless of what you thought about the companies in question, about their stock price, their products or their management teams… If you did that, you’d be on to something very powerful. This is what we call the momentum strategy: a variant of trend following that seeks to systematically pick top performing stocks and hold them for as long as they outperform. How well does this strategy work? A very extensive empirical study covering over a century of data showed just how well momentum investing performs.

London Business School researchers Elroy Dimson, Paul Marsh and Mike Staunton analyzed stock price history starting from the year 1900. They constructed investment portfolios by selecting 20 top performing stocks in the previous 12 months from among the UK’s 100 largest publicly trading firms, and compared their performance to portfolios of 20 worst and 60 middle performers, re-calculating the portfolios every month.

They found that the lowest-performing stocks would have turned £1 invested in 1900 into £49 by 2009. By contrast, the top performers would have turned £1 into £2.3 million, a 10.3% difference in compound annual rate of return over a 109-year period! When they included in their study ALL of the London stocks from nineteen-fifty-five onwards, the gap was even wider: the top quintile generated a compound annual rate of return of 18.3% versus 6.8% return for the bottom quintile.

The researchers found the strategy to be “striking and remarkably persistent.” It proved successful in 17 out of 18 global markets studied, with data going back to 1926 for North America and to 1975 for larger European markets. The only exception was Japan, where the results were based only on the post-2000 data – the period that coincided with a protracted bear market in Japanese equities.

Thus, Dimson, Marsh and Staunton included a massive chunk of stock market history across 18 global stock markets and gave us irrefutable evidence that trends really are the most potent driver of investment performance over the long term. This principle has held true through the two world wars, the 1930s depression, 1970s inflation, Korean War, Vietnam War, the collapse of the Communist Block, the rise of China, 911 terror attacks and the global war on terror. The century covered by this study has been one long roller-coaster for the global capital markets and through all of it, powerful trends prevailed as dominant drivers of investment performance.

Trend following vs. value investing…

Now, it is true that for many people trend following is still a bit counterintuitive and difficult to accept as it involves buying assets only after their prices have already appreciated considerably and selling them well after their price has peaked. By contrast, value investing seems much more appealing since it involves shopping for investment bargains and buying assets at low prices.

Moreover, value investing has been championed by Benjamin Graham and Warren Buffett, two of the most successful investors ever. Well, here again we’ll fall back on one of our pillars of long-term success at investment speculation: TRUTH – and the truth is that both Graham and Buffett owe their success entirely to momentum investments rather than value picks. If that assertion seems sacrilegious, I’ve laid out the case in this article here.

Alex Krainer – @NakedHedgie has worked as a market analyst, researcher, trader and hedge fund manager for over 25 years. He is the creator of I-System Trend Following, publisher of TrendCompass reports and contributing editor at ZeroHedge based in Monaco. His views and opinions are not always for polite society but they are always expressed in sincere pursuit of true knowledge and clear understanding of stuff that matters.

BOOKS & LINKS:

- “Alex Krainer’s Trend Following Bible” (2021)

- “Grand Deception: The Truth About Bill Browder, Magnitsky Act and Anti-Russia Sanctions” (2017) twice banned on Amazon by orders of swamp creatures from the U.S. StateDepartment.

- “Mastering Uncertainty in Commodities Trading” (2016) was rated #1 book on commodities for investors and traders by FinancialExpert.co.uk

- WEBSITE: ISystem-TF.com

- BLOG: TheNakedHedgie.com

- YOUTUBE CHANNEL: MARKETS, TRENDS & PROFITS

- LinkedIn: linkedin.com/in/alex-sasha-krainer-0b74ab1a

I agree with most of the reasoning of the article. But the title exaggerates the facts, based on anecdotal evidence. Taking the broad averages of well constructed benchmark indices of SG Trend and S&P500 TR from the inception of the younger SG Trend at the end of 1999 to the end of 2022, they only give almost the same performance of 6,4 and 6,6 % p.a., respectively.

This result is also supported scientifically by the Grossman Stiglitz Paradox that well informed professional active investors – such as trend followers with managed futures – expect a compensation for their extra efforts beyond the market return adequate to this return. Nothing more and nothing less! Otherwise they would trade more or less until they achieve this compensation on average over the long-term. This keeps both the stock and the trend markets as efficient as possible.

Thus, professional trend following, which I believe the SG Trend is representing well, should provide a similar return as broad stock indices on average over the long term of decades, as my comparison shows. And as they develop in a truly non-correlated way trend and stocks combined outperform both investments alone thanks to rebalancing alpha. But again both trend and stocks contribute similarly to that.

This is good news enough and would convince more investors than anecdotal exaggerations. Just my five cents as true believer in indexing both stocks as well as trend, one of the optimal ways for long-term investment success. Stock and fund picking is a looser’s game on average. 😉

LikeLike

Hi Norbert – thank you for that feedback; in fact, your remarks are very legitimate and I’ll take them into account.

LikeLike