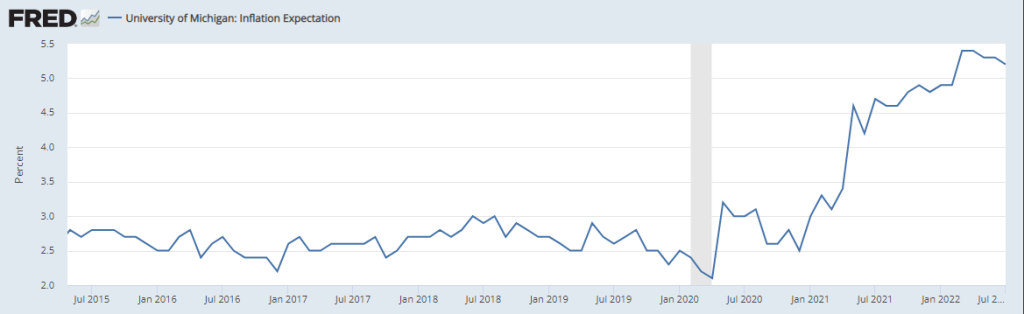

Inflation expectations in the US have tapared off since May, but inflation genie won’t be put back into the bottle easily.

The chart above shows University of Michigan Inflation Expectations. While it’s soared from 2021, it peaked in April and May 2022 and started to come down since then. But let’s take a slightly longer view of this process.

In 2020, the problem was too little inflation

In the year 2020, a long, long time ago I published the article, “The Coming Inflation Tsunami and How to Protect Your Portfolio,” warning that inflation could burst forth suddenly, with devastating effects for savers and investors. In 2020 the policymakers’ chief challenge was how to ignite inflation. At the time, inflation had been all but dead, stubbornly unresponsive to policymakers’ efforts to lift it to their 2% target. So the brightest monetary minds decided let inflation loose beyond 2% and then “hit the target from above.”

Well, the first part of that plan is on track and we’re well above target. But the second part will prove extremely difficult. Abundant historical record shows that price inertia tends to be very strong; inflation is hard to ignite, but once ignited, it is hard to control. Three main variables determine prices in an economy:

- Money supply

- Velocity of money, and

- Supply of real values

Monetary authorities can only control one of the three: the supply of money. Since the beginning of 2020 and justified by the Covid 19 pandemic, central banks have radically increased the amount of money in circulation. In the US, the M2 money supply soared from $15.3 trillion in February 2020 to $21.6 trillion today (as of August 2022), a staggering 41% increase in just over two years! The velocity of M2 collapsed, from 1.37 in Q1 2020 to 1.1 in Q2 2020.

The 2020 collapse was no surprise: money velocity is a simple ratio of the nominal GDP to the M2 money stock. A large increase in M2 will depress this ratio as it won’t immediately have any significant impact on the GDP. But today the money velocity is starting to turn up. The velocity of money measures how many times a unit of currency is used to purchase domestically produced goods or services during some time interval. The more often money changes hands, the greater its velocity.

Sow the wind, reap a storm

Because velocity of money is determined by the aggregate psychology of the economy’s participants, which is only slow to react to changing conditions in the economy, it tends have a strong inertia that’s beyond monetary authorities’ control. If people lose confidence in their currency because it is rapidly losing purchasing power, they’ll seek to get rid of it and to exchange it for items of real value. That increases money velocity and in turn adds upward pressure to inflation.

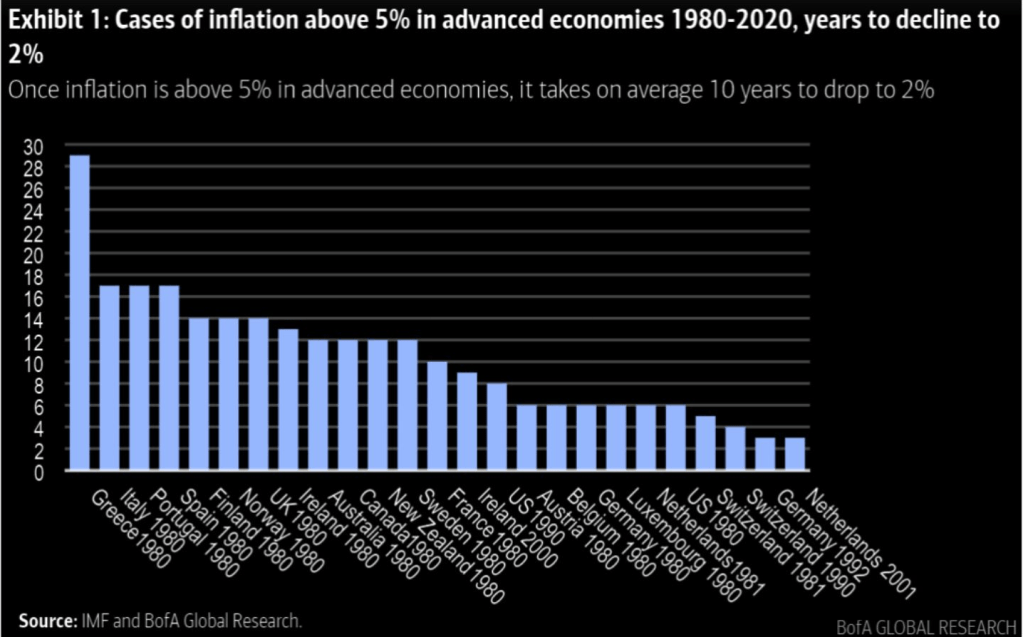

When Japan’s minister of finance Korekyo Takahashi (1931-1936) resolved to stoke a bit of inflation to break Japan’s deflationary rut 90 years ago, he also thought that he would be able to control inflation at reasonable levels. He was wrong and what he got was hyperinflation. In fact, that’s what usually happens when governments or central banks ignite a little inflation: it tends to overflow. Research from Bank of America Global Research suggests that once inflation breaks above 5%, it takes on average ten years for it to drop back to 2%. During that time, inflation often runs much hotter than 5%.

If anything, the above chart might be downplaying the problem: on the right it shows “US 1980,” suggesting that once inflation exceeded 5%, it took 6 years for it to drop back down to 2%. BofA used IMF data, but not all would agree:

According to the US Bureau of Labor Statistics data as presented in the above chart, US inflation burst above 5% in March of 1969 and only fell back close to 2% in March of 1986. By my calculations, that’s fully 17 years, not six!

Incidentally, there’s another important aspect to the above chart: it shows inflation advancing in three distinct waves before it finally ran its course. We could see a similar progression this time around as well as acceleration of inflation gives way to an easing, only to advance to another great leap forward.

Wealth destruction

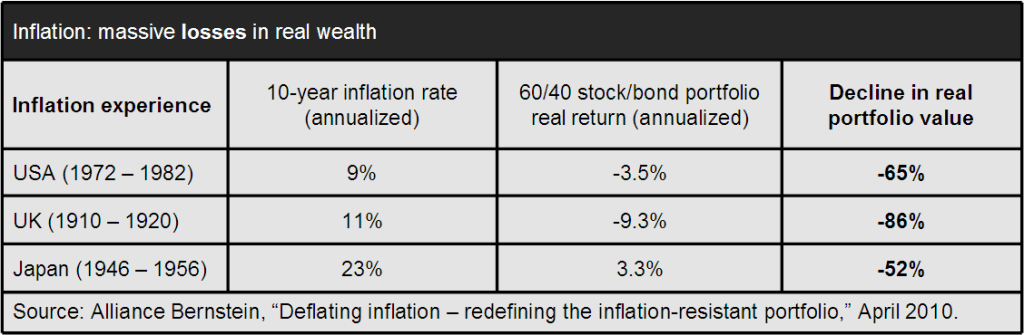

In his seminal paper, “Modern hyper- and high inflations,” Stanley Fischer found that since 1960, over 2/3rds of world’s market economies experienced episodes of inflation exceeding 25%. During such episodes, investors on average lost 53% of their savings’ purchasing power.

During the 1970s inlfation in the US, which averaged about 9%, American investors lost 65% of their wealth in real terms (based on the performance of a typical 60/40 stocks/bonds portfolio). But in many cases, the inflation-inflicted losses were much worse, approaching 100%.

Defence against dark arts

Today, the economies of Japan, Great Britain and Europe are on the same historical trajectory where inflation will likely take many years to run its course, inflicting severe damage to savers and investors. Even the US economy won’t be able to escape a bad inflationary episode. The next question is, what to do about this?

Empirically, the best defence against dark monetary arts is to gain meaningful exposure to a diversified basket of commodity prices including energy, precious and industrial metals as well as agricultural commodities. You can find further details about such portfolios on this page or in this PDF document.

However, such investments may require a fairly large asset base and remain out of reach of most investors. For smaller investors, perhaps the best protection would be to acquire some physical gold and silver, and if at all possible a plot of arable land. Farmland is the second best inflation hedge, and if you know how to use it, can double up as a source of sustenance.

Things that are NOT effective inflation hedges are investments in stocks, bonds or real estate (except farmland). That’s beyond this article’s scope, but I will elaborate on this in the near future.

Sign up for a 1-month free trial of I-System TrendCompass!

One of the best trend following newsletters on the market, I-System TrendCompass delivers consistent, dependable and effective decision support daily, based on I-System trend following strategies covering over 200 key financial and commodities markets with no dilution in quality or focus.

- Cut the information overload

- Get real-time CTA intelligence in seconds per day

- Never miss a major trend move

- Navigate trends profitably, with confidence and peace of mind

One month test-drive is always on us. Sign up for a 1-month FREE trial by e-mailing us at TrendCompass@ISystem-TF.com

To learn more, please visit I-System TrendCompass page.

One thought on “Inflation is here to stay”