This is not a hollow boast. While I-System has generated superb performance over the years, the key reason for this claim reflects a higher-order quality of the model: I-System has the potential to entirely transcend uncertainty and largely replace the human factor in asset management in a broad variety of investment strategies including portfolio allocation, momentum, CTA, tail risk and equity long/short .

To earn profits, investors must take and manage risk. In modern times we usually think of risk taking in terms of stocks, high yield bonds, private equity or hedge funds. To strip out the complexity of today’s market instruments, let’s turn back the clock five centuries and look at risk in its raw form.

After the 1492 discovery of the New World, adventurers could earn high returns on investment by sailing across the Atlantic and plundering Mayan, Aztecan or Incan treasures. The riches discovered in Peru were so great, that “…the like of which past centuries have never seen, nor do I think that the coming ones will believe.”[1]

Across Spain, young men were stirred by “flaming pictures of an El Dorado where the sands sparkled with gems and golden pebbles as large as birds’ eggs.”[2] Over the following century, an estimated 240,000 sailors, tradesmen and adventurers risked everything to join the enterprise and seek their fortune. One of these adventurers was Pedro Cieza de Leon; he was enticed to cross the ocean after he witnessed a large cargo of Inca gold being unloaded in Seville: “As long as I live,” wrote Cieza de Leon, “I cannot get it out of my mind.”

Adventurer’s risk

To finance the crossing, adventurers turned to wealthy tradesmen and bankers: it was necessary to secure a seaworthy vessel, adequate provisions of food, spare materials, tools and weapons, and a capable captain and crew. A successful round-trip crossing could yield a huge payoff, but the risks were significant.

Apart from succumbing to disease or injuries, the voyage itself was very dangerous. Encountering a risk event like a tropical storm or a hurricane often entailed total loss.

Among maritime merchants, it has always been well understood that with good weather, even amateurs on a shoddy vessel could cross the Atlantic safely. But hurricanes could sink even the best built ships under most experienced crews.

This principle remains valid in modern investment management: the success of your strategy depends on the market conditions you encounter. In favourable conditions, even mediocre managers can do well: if you are a long-only stock investor in a bull market, or if you run a short bias fund in a bear market, you’ll be successful. Among trend followers, even very simple trend following strategies will do well when markets are trending. But during reversals, or a prolonged absence of trends, even the best managers might fail.

Expectancy and the psychology of trading in modern investing

Remember, all decisions are made on the basis of models. … The heart of the matter is your relative degree of confidence in each of these models.

Jay W. Forrester

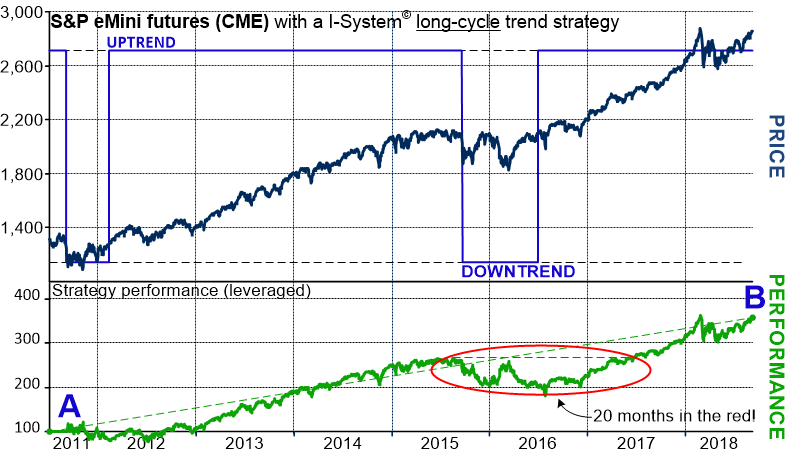

Expectancy is the answer to the question, “what happens if I continue doing this?” This deceptively simple question is critical in investment speculation, where “doing this” implies using some investment strategy. In systematic trend following, we strive to use strategies that have a positive expectancy based on their past performance. However, when analyzing that performance, we tend to collapse time into a snapshot of history. Consider a typical I-System Trend Following strategy illustrated below:

From 2011 through 2018 this strategy generated a compound return of just over 20%. But its long-term performance between points A and B in the above chart can’t convey the day-to-dayexperience of making and losing money. This experience can have decisive psychological effects. For example, if you were unlucky to implement the above strategy around mid-2015, you’d have to persevere through nearly a full year of draw-downs and sit out 20 months of negative performance.

You would only be able to do this if you had utmost confidence in your strategy. Watching your losses mount for that long can make the urge to change course irresistible: you might abandon the strategy or replace it with one that would look better at the time. But this could be a costly mistake: you might abandon a strategy that’s near the end of its losing streak, depriving yourself of the gains that would follow.

Worse, you might replace the strategy with one whose losing streak was about to begin. In investment management, this is called strategy drift, one of the great pitfalls in active investment management. Even with well-formulated, positive expectancy strategies, sustaining high investment returns depends on our ability to tolerate extended drawdowns without altering course. This may well be the most important lesson to master in investment management.

In adversity, quality is decisive

Returning to our ocean-crossing metaphor, we can think of drawdowns as the investing equivalent of sailing through a storm. The survival of the vessel and the crew hinges on three key elements: (1) the quality of the ship and the equipment, (2) captain’s leadership, and (3) the performance of the crew.

- The quality of the ship: captain’s, crew’s, and the cargo owners’ confidence that the ship is well-built and capable of withstanding adverse weather makes it possible for everyone to proceed with composure and focus on doing what needs to be done. In investing terms, the ship and equipment are the equivalent of the models and tools of portfolio management.

- Captain’s leadership: the captain directs the ship to its destination. His role is pivotal, particularly through adverse conditions. If the crew lost their faith in his good judgment, they might disobey his orders and abandon their posts. The odds of that ship surviving through a storm would collapse.

- Performance of the crew: the ship is more likely to arrive at its destination if all hands diligently perform their assigned tasks, regardless of how bleak the situation might be at any given time. The crew’s ability to do so depends on their confidence in their captain’s leadership and the quality of the vessel they are operating.

Thus, any venture’s success depends on a sustained positive interaction among all three of these elements. These issues address the question of quality and risk at the level of an individual venture or strategy. But another powerful way to reduce risk is diversification across multiple ventures as we discuss next.

Diversification: the next level in risk management

Diversification is probably the most effective way to mitigate risk. Staying with our maritime analogy, suppose that you financed a single crew sailing across the Atlantic. Even if you put together the finest ship ever built with the best crew money could buy, a powerful hurricane could still sink it and inflict a total loss on the venture. But if, instead of gambling on the success of one ship you could acquire say, a 20% interest in 5 such ventures, your investment could pay off even if one of the vessels sank along the way.

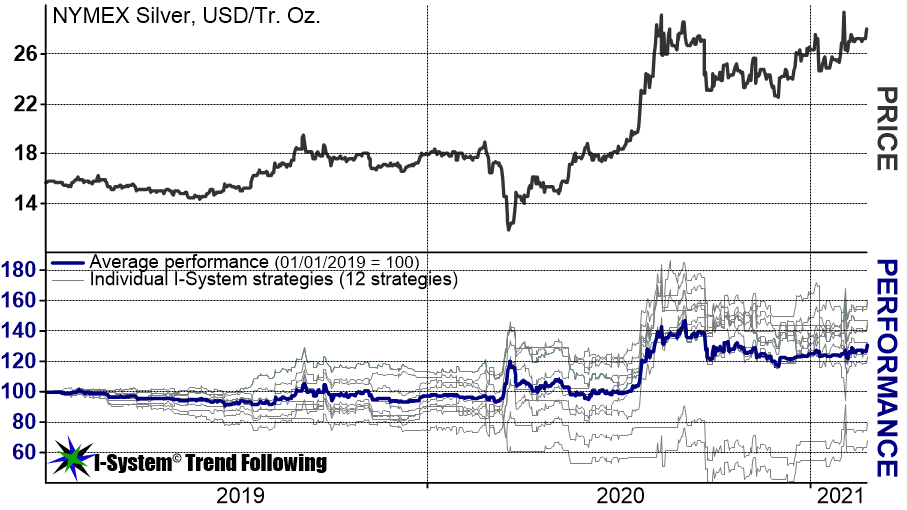

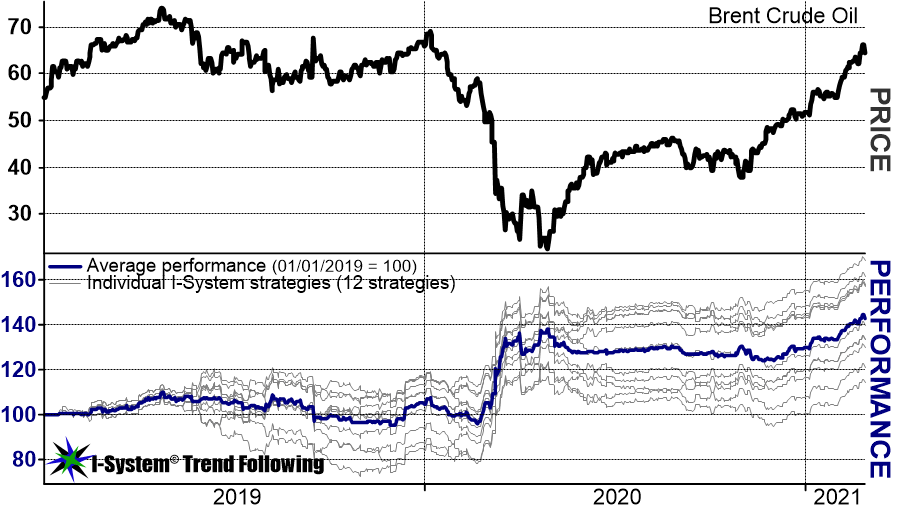

Below is the trading equivalent of this principle: the following chart shows the performance of 12 I-System COMEX Silver strategies which illustrates this idea:

Our Silver strategies have performed very well over this period in spite of two of them doing relatively poorly. A well diversified set of trend following strategies can withstand a few laggards among them: the average performance of this small swarm is more reliably positive than any individual strategy could be.

In fact, fragmenting risk among multiple strategies (navigation paths) is the common sense approach to reducing risk. People do this by allocating their assets between stocks, bonds, real-estate, precious metals and other asset classes. Large asset managers do it by allocating capital to multiple portfolio managers pursuing different investment strategies. Even if one of the strategies fails or underperforms, others may succeed, improving the expectancy of the overall investment portfolio.

I-System: quality, performance, diversification – all-in-one

What’s needed is a sound intellectual framework for making decisions and the ability to keep emotions from corroding that framework

Warren Buffett

In creating the I-System we sought to build an effective solution to all of these problems. At the level of an individual strategy we endeavoured to craft the best possible method of formulating trading strategies and to “industrialize” this process so that we could generate a large number of high quality strategies with positive long-term expectancy. At the outset, this seemed like an impossibly ambitious objective, but by 1999 we had a working prototype of this model and by 2003 we completed its industrial strength version – the model we have used daily ever since.

Closing the conceptual framework: systematic trend following

One significant challenge with quantitative research stems from an overabundance of data and computing power offering an unlimited universe of possibilities to analysts. This rendered the very search for high conviction strategies a time consuming, resource intensive and risky. Here are a few examples of junk that lurks in big data:

To avoid these pitfalls, we deliberately limited I-System’s range of speculative behaviors by fixing the knowledge framework within which we could formulate trading strategies. We spent more than two years testing a large variety of algorithms to determine which of them added value. We selected those and eliminated all others to keep the model’s complexity manageable. Through this process, our thinking converged on trend following as probably the best way to capture value from unpredictable price fluctuations. In terms of our seafaring metaphor, you could say that we simply limited the range of destinations our ships could sail toward.

Coding issues and model risk

By the time we completed I-System’s prototype, we realized that there could be many errors in its code. Certain kinds of errors can go undetected for a long time until something goes wrong. Rather than venturing to trade with potentially flawed equipment, we decided to hire the best software talent we could find and to rebuild the I-System with strict adherence to best practices in software engineering. We did that not once but twice: in addition to the prototype we built two new versions of the model and ran them in parallel until we were satisfied that for the same inputs, all three versions produced identical outputs. This was a fastidious process, but it was the only way for us to be sure that we had eliminated all the coding errors and reduced I-System’s model risk near zero.

Fragmenting risk within a fixed strategy framework

Life can only be understood backwards; but it must be lived forwards.

Søren Kierkegaard

Our next problem was uncertainty about any strategy’s future performance. Even today’s top performing strategies could have a bad losing streak in the near future. The only robust solution to this problem is to fragment risk across many different strategies, so we designed the I-System as a parameter-driven knowledge framework that we could use to formulate hundreds of strategies in any market. As a result, I-System can accommodate a very wide range of speculative behaviors within that knowledge framework: each strategy’s trading is determined by the same fixed algorithms, but varies according to some 70 different calculation parameters.

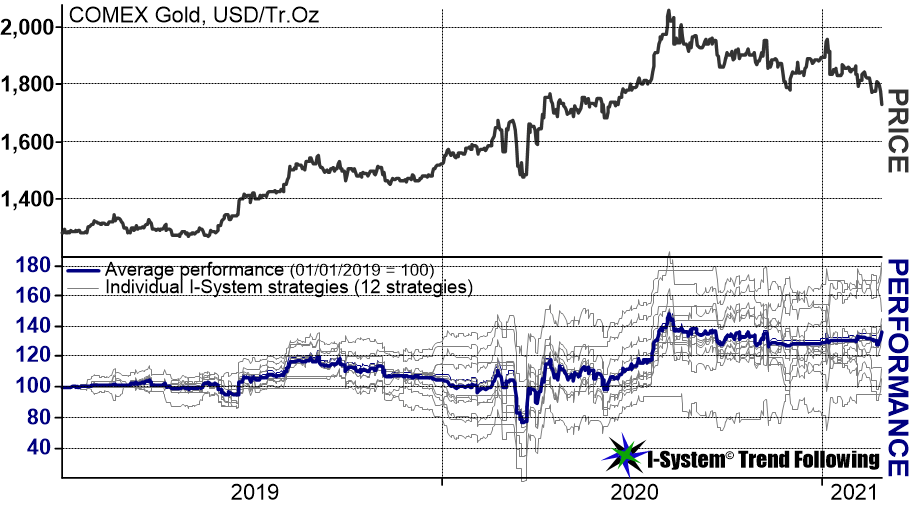

The importance of this capability cannot be overstated: it is the key reason we believe I-System is the very best trend-following model ever built. By using a multitude of strategies, the average performance will tend to converge on the model’s intrinsic quality, even if some strategies underperform. The following two charts illustrate the idea once more:

The above chart shows the performance of a dozen I-System strategies on COMEX Gold. While two of them finished the period with a loss, ten others generated significant trading gains making the average performance robustly profitable. We’ve observed this effect consistently over time and across markets:

A performance update summarizing the results of our Major Markets portfolio comprising 180 markets in 15 key global markets is at this link.

Speed matters

Building the I-System was indeed a hugely ambitious project and it is a matter of great pride that we have been entirely successful with it. In addition, we have been able to enhance the model’s calculation speed by over 40 times: our prototype took between 3 and 4 seconds to calculate a single back-test simulation. The professionally engineered version can complete more than 40 such simulations in that time. When your fitness landscape consists of 1070 possibilities, speed makes a critical difference: I-System can search that fitness space with an efficiency that’s orders of magnitude beyond the capabilities of lesser quantitative models. Achieving such process optimization requires highly advanced software engineering skills which aren’t taught to quants typically employed in finance industry.

Effectiveness

Q: But how do you know that the model you have created is right?

A: There is no proof that Einstein’s theory is right. There is no proof that Ohm’s law in electricity or Boyle’s law in gasses are right. There is only an experimental demonstration that such laws are useful for specific, limited purposes. There is no way of proving that a model or law or theory representing the real world is right.

Jay W. Forrester[4]

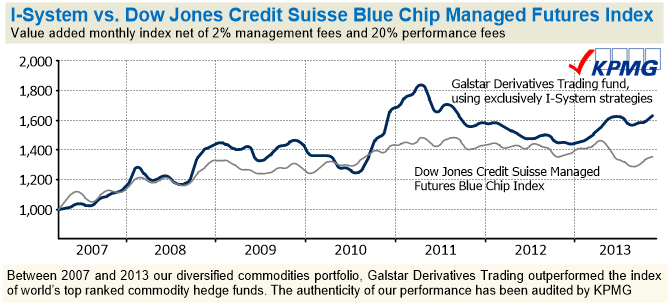

We designed the I-System as a solution to the problem of uncertainty: a way to navigate unpredictable market fluctuations profitably. But when we build any model, we can’t be certain that the model is valid. What we can do however, is to demonstrate that it performs the function it was intended for. With the I-System, we have demonstrated this in the most rigorous way possible: we used it since 2007 to manage several investment funds, tracking hundreds of individual strategies.

From 2007 to 2019 we have consistently outperformed our relevant benchmarks including the world’s top-rated CTAs as tracked by the Dow Jones Credit Suisse index of Blue Chip Managed Futures funds. Between 2011 and 2019 we used I-System to run a tail-risk strategy under Altana Inflation Trends Fund. During that time we outperformed the EurekaHedge tail risk index.

This long and rigorous testing of the I-System gave us robust evidence that I-System is indeed a valid answer to the problem of uncertainty. Outperforming even the best among our peers gave us reassurance that I-System is at least as good as the models used by the world’s leading CTAs.

The ultimate prize: transcending uncertainty

But these large managers employ dozens, and in some cases hundreds of quants to manage their trading models. By contrast, I-System works through one knowledge framework. It can track a virtually unlimited number of investment portfolios and trading strategies in any security market[5] with no dilution of quality or focus.

I-System’s ultimate potential is to transcend uncertainty altogether – not by predicting future outcomes, but by replacing uncertainty with a more predictable asset class: a swarm of autonomous intelligent agents that generate positive expectancy decisions with utmost consistency, free from emotion or distraction.

The road ahead

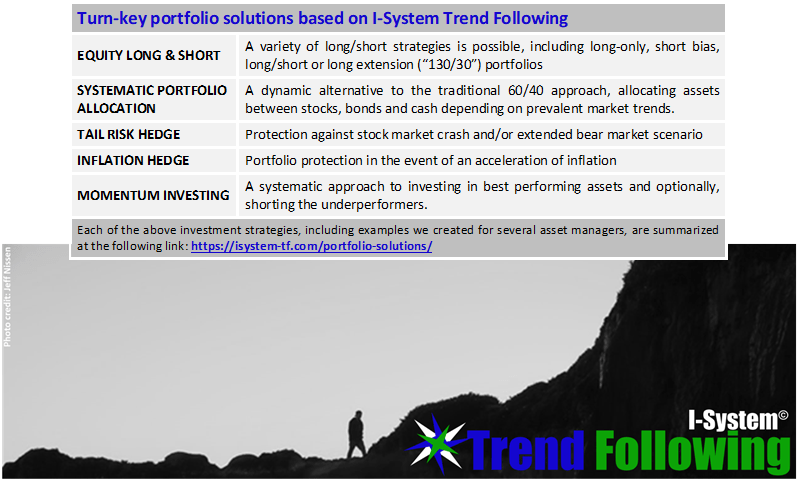

Fintech revolution has created new opportunities for independent solution providers in the financial industry and Krainer Analytics is well placed to deliver effective and reliable portfolio solutions for investment managers and hedging solutions for firms with significant exposure to FX and commodity price risk. Importantly, our solutions will prove cost-efficient, since they can replace many human experts who still constitute one of the highest expense items in such organizations. Thanks to the I-System, Krainer Analytics can today offer quality turn-key portfolio solutions for the following investment strategies:

Notes:

[1] From the “Historia del emperador Carlos V” (1545) by the contemporary historian, Pedro Mexia.

[2] W. H. Prescott, “History of conquest of Peru” – 1843.

[3] This is according to a multi-year study of 13,000 programs by Watts S. Humphrey of Carnegie Mellon University’s Software Engineering Institute.

[4] In an interview for McKinsey Quarterly; Jay W. Forrester was the Germeshausen Professor Emeritus at MIT.

[5] Provided that the market has sufficiently long history (at least 10 years of price data) and volume

3 thoughts on “I-System: probably the best trend following model ever built”