Last week Bank of America published another market report, helpfully summarized by ZeroHedge. BoA’s chief market strategist Michael Hartnett has been turning increasingly bearish and expects that a coming [interest] “rates shock” will burst the asset bubble. This is in fact very much possible and there’s a 50% chance that Hartnett is right (heads, he’s right – tails he isn’t) but the charts in the report are extremely interesting:

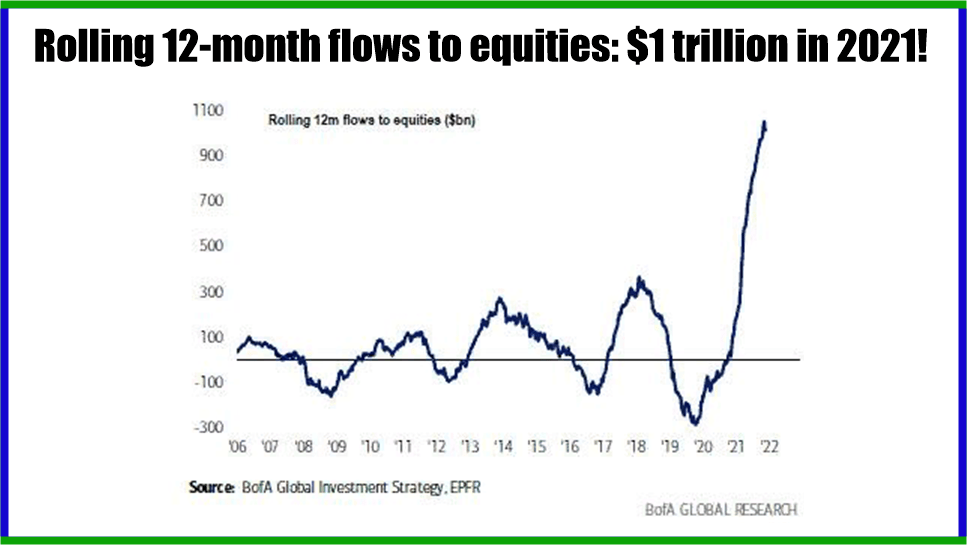

This confirms what we already knew: that the Fed’s unprecedented monetary inflation largely flowed toward the capital markets. In fact, monetary inflation is the principal driver of asset prices, and this is nothing new. In my article, “The One Force Moving Stock Prices and What it Tells Us About the Future” I’ve summarized the boom-bust cycles data since the 1920s which shows the close correlation between monetary expansion and stock prices.

Incidentally, capital markets represent one of the two great inflation absorbing reservoirs, which explains why the unprecedented quantitative easing hasn’t caused high rates of consumer price inflation for so long. The other inflation reservoir are trade deficits, the mechanism that effectively exports a nation’s inflation to her trading partners who then recycle their trade surpluses into capital markets.

Michael Hartnett’s bearish case is indeed compelling and hard to dismiss. However, there’s also a 50% chance that Scott Rubner‘s bullish case is right. Goldman Sachs’ funds flows analyst recently noted that over $15 billion in “non-fundamental equity demand” is continuing to flow into the markets daily and suggested that “We are entering the best seasonal trading period of the year…” Rubner then asks: “What happens if there are no outflows in 2022 and global equity inflows continue?” In fact, there’s a good chance that this is exactly what we’ll see over the coming months, further inflating the US asset bubble. It’s what we saw in many historical episodes where stagflation + monetary inflation resulted in massive asset bubbles (Weimar Republic in 1922, Israel in the 1980s, Zimbabwe, Venezuela, Argentina, etc.).

So in spite of the fact that we are indubitably in a bubble of massive proportions, betting against it is always a risky proposition. One of the most memorable examples where a seasoned money manager burnt up his fund by shorting equities in the middle a bubble happened at the peak of the dotcom era in 2000. Stanley Druckenmiller, one of Jack Schwager‘s original “market wizards,” built up a large short portfolio that included many of the silly but staggeringly inflated dotcom loss-making machines.

Then as now, there were compelling “fundamentals” arguments suggesting that the market would crash. But unfortunately for Druckenmiller, in just the last 5 months of that bubble, the Nasdaq rallied fully 110% and his portfolio was bleeding losses. Literally at the last moment (only one hour from the market top) he lost his nerve, closed out the short positions and joined the herd right over the cliff.

During the following six weeks he lost about half his fund while most of the equities he’d previously shorted collapsed by between 90% and 100%. The year 2000 should have been spectacular for him, but instead he suffered the worst loss of his career. Druckenmiller wasn’t wrong: he only made the mistake of betting against the trend. This story is one of the most fascinating cases of psychology of speculation, which I outlined it in more detail in this article, including Druckenmiller’s own account of the way it went for him.

From today’s perspective, there can be little doubt that that the current bubble will ultimately burst. However, betting against it too soon is a risk I would not recommend even for today’s silly loss making machines (which dwarf their dotcom predecessors), to say nothing of the surging ranks of corporate zombies.

Instead, it would be more prudent for investors to navigate events by using a set of quality trend following strategies: they’ll keep you on the right side of the bull market all the way to its peak, which could be considerable ways away. And while trend following won’t get you out of the market at its peak, they’ll signal the shift into the bear market in due course, whereupon you can continue to profit through the bear cycle. Below is how we navigated the last boom-bust cycle:

I-System Trend Following provides superbly engineered portfolio solutions and daily decision support through I-System TrendCompass – real-time CTA signals covering over 200 financial and commodity markets. For more information and to sign up for a 1-month free test-drive, please visit the TrendCompass page or e-mail us at TrendCompass@ISystem-TF.com

Thank you

i need to move my money from banks possibly

LikeLike