With all that’s going on in the world, worrying about your investment portfolio may seem like a distraction. Over the last few years the issues of politics, public health and war took the spotlight. Still however, managing our savings and safeguarding their purchasing power must remain a central concern; as Doug Casey put it in a recent interview on Geopolitics & Empire, preserving your wealth could be the single most important priority. As Alexander Hamilton put it, “In the general course of human nature, a power over a man’s subsistence amounts to a power over his will.” This is true today as it has been for ages: losing your wealth, however great or small, means losing freedom, and becoming prey to the malevolent powers shaping the new global order. It is not for nothing that they want us to own nothing.

The rise in inflation is rendering this challenge ever more difficult, since it predictably and indiscriminately diminishes the purchasing power of savings.

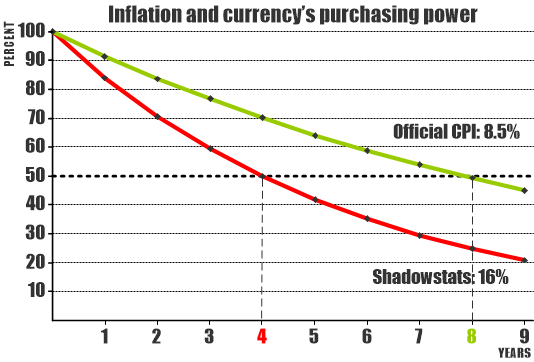

At the current official rate of inflation (CPI), it will take less than 9 years for US dollar’s purchasing power to halve. More realistic inflation rate, according to John Willams’ Shadowstats is now about 16%. At that rate, the dollar’s purchasing power will halve in only four years. Other western economies are experiencing similar or worse inflation levels. As I elaborated in an earlier article (see link), even if inflation eases off a bit in the coming months, high inflation will be with us for years.

So, what can we do to protect the purchasing power of our savings? Opinions are many and varied, but for the most part they cover investing in stocks, inflation-protected bonds, real estate, gold, silver and Bitcoin or other cyrptos. But not all of those are effective inflation hedges. As I elaborated in “The Coming Inflation Tsunami and How to Protect Your Portfolio,” empirical evidence is quite conclusive: the best possible way to protect yourself from inflation is to gain meaningful exposure to commodity prices (i.e. not just gold and silver, but a diversified basket of commodities including energy and agricultural commodities).

Unfortunately, gaining exposure to a diverse basket of commodities might be quite a challenge for most investors. In an industry structured entirely around stocks and bonds investing, there are few quality options available to investors and DIY approach throws us up against the problem of uncertainty. Who knows enough about heating oil, copper, cotton, coffee, wheat or frozen orange juice to risk trading in those markets? Very few of us indeed, but that’s where the good news comes in: you don’t need to know anything about those markets to trade them successfully.

Trend following: your best defense against monetary dark arts

All you need to learn about is trend following, and this is no exaggeration. I’ve traded successfully in over 50 different financial and commodities markets and I don’t know the first thing about most of them. Rather than studying the fundamentals of each market, I studied trend following which is applicable in all markets, including stocks, bonds, commodities and currencies. But it’s better than that: not only does trend following “work” in any market, it is in fact more effective and more reliable than the conventional approaches to security analysis. After more than 25 years working as a market analyst, researcher, trader and hedge fund manager, experience has led me to formulate two simple hypotheses that form the philosophical foundations of I-System Trend Following:

- Market trends are far and away the most powerful drivers of investment performance,

- Systematic trend following is the most reliable way to capture value from trends.

Each is elaborated in articles at the links and as you’ll find, they are quite hard to argue with.

The proof is in the pudding

Real-world evidence corroborates the validity of these hypotheses, as the following chart shows. It compares the performance of the Societe Generale CTA index with the Bloomberg US Aggregate Total Returns Value index:

The Bloomberg index is a broad-based flagship benchmark that includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate pass-throughs), ABS and CMBS (agency and non-agency); SocGen CTA index measures the performance of CTAs, Commodities Trading Advisors. As a rule, CTAs are trend followers; they speculate in a wide variety of financial and commodity markets and tend to rely on following models for directional exposure and trade timing.

CTAs are all active investment managers and they all report their performance results after fees. In trading financial and commodity futures, they merely speculate: those instruments generate no interest yield and no dividends. There is a lot to read into the above chart. The fact that CTAs outperformed the Bloomberg index as a group is actually quite amazing, but we should also recognize the challenge faced by the CTAs and all other investors.

The performance curves make it clear that trend following isn’t a magical ‘straight-line-up’ solution to the problem of investment speculation – the reason I frequently harp on two important requirements for success in investment management: discipline and patience. As the chart shows, CTA performance has had an uneven trajectory that included many run-ups, draw-downs and several long periods of sideways drift. Indeed, periods of flat/negative returns span much of the interval from 2009 through 2020 – the period that coincides with the unprecedented central bank QE experiment which has resulted in gross distortions of the market-driven price discovery process.

One of the curious distortions of this period included a decade-long period of flat commodity prices as I elaborated in last year’s article, “Trend following: why it fell from grace and why it’s coming back.” The absence of those price trends explain CTAs flat/negative returns intervals. One notable exception was the strong 2014 run-up which coincided with the 55% collapse in commodity prices in 2014 and 2015.

But there is a broader reason why CTA outperformance is a rather spectacular fact: we have now reams of empirical evidence showing unmistakably that a vast majority of active asset managers underperform their strategy benchmarks. Namely, in any given year about two thirds of them underperform, but over longer intervals (5-10 years), more than 90% of them underperform.

Furthermore, CTAs achieve their results by simply following market trends. They ignore market fundamentals, econometrics, narratives, and all the Cartesian analyses and research that keep other asset managers busy day in and day out. Another important facts emerging from the above chart is that during market downturns, trend followers tend to be inversely correlated to conventional asset classes, delivering positive returns exactly when investors need them the most.

I believe these are very compelling arguments in favor of trend following based on decades’ worth of empirical evidence. The fact that these arguments are still disputed or dismissed in the financial services industry (often with derision and scorn) is a testament to the mindset barrier (excerpted below), rooted in misguided groupthink. It is also why I wrote in the past that trend following is to portfolio management as arabic numerals are to mathematics.

The mindset barrier

In spite of the undeniable success of trend following strategies, most investors continue to regard trend following as an oddity, not entirely fit for the ranks of serious market professionals. The reason for this has nothing to do with performance but is in part simply cultural. Namely, most of today’s market professionals were educated in the Cartesian tradition which validates rigorous scientific method as a way to acquire knowledge. Value is placed on understanding linear cause-and-effect relationships that allow us to make predictions about stuff. This mindset has an obvious appeal in investment speculation: we expect to predict and profit from market events by understanding how the conditions we observe would cause them. That mindset also gives us the comfort in the sense of competence and control.

Trend following is a cultural misfit in this intellectual tradition. To begin with, it is based on a field of study called technical analysis where knowledge accrues through judgment heuristics and experience rather than empirical science. Trend following also blurs the relationship between intellectual work and its expected results. The linear thinking investor judges a transaction according to an explicit understanding of how and why that transaction should generate a profit. The trend follower simply implements a set of predefined rules, accepting that any given transaction may produce a loss. A trend follower expects profits, not from any particular transaction, but from a long sequence of trades extending far into the future.

Thus, while the conventional approaches to investing stem from an understanding of a particular situation, trend following is based on the belief that a certain predefined speculative behavior will deliver positive results over time, regardless of the economic situation, industry, market, or geography. Incidentally, this is another great advantage of trend following: if you learn how to read the charts, or formulate high quality trend following strategies, you’ll be able to greatly enhance your universe of opportunities.

By understanding trends, you’ll be able to trade securities even if you don’t know everything about them. As I said, I’ve traded in well over 50 different financial and commodities futures markets and I know next to nothing about most of them. I merely believe that they move in trends and that with a disciplined adherence to a well-formulated set of rules I’ll be able to capture profits from such trends as and when they emerge. Experience and results have proven me right.

Using trend following with small portfolios

For most investors, one challenge with trend following is the requisite size of a portfolio. To create a well-diversified portfolio including energy, metals, agricultural commodities, foreign currencies and also stock and bond instruments may require a fairly large asset base. A single crude oil futures contract entails trading 1,000 barrels of oil; a contract of gold 100 troy ounces, a contract of wheat 5,000 bushels, etc. But today, investors can resort to mini- or even micro-contracts for many of these markets. Another solution is to invest in ETF (exchange-traded funds) that provide a proxy to exposure to oil, gold, copper, etc.

Further resources

Internet is full of helpful materials that can help you learn more about trading commodity futures and about trend following. However, do please beware of gimmicks that promise unrealistic profits or things like 80% or 90% profitable trades – these are sure to disappoint. The I-System Trend Following website provides the following books and resources:

- Free download: “Mastering Uncertainty in Commodities Trading“ (2016) which was rated #1 book on commodities for investors and traders by FinancialExpert.co.uk

- Another free download: “Alex Krainer’s Trend Following Bible“ (2021) – this title got no awards, but it’s a more recent material, and probably a better quality text.

- Seven simple do’s and dont’s of systematic trend following

- I-System TrendCompass – our daily trend following newsletter covering over 200 financial and commodities markets (one month’s subscription is always free of charge).

Finally, apart from active portfolio management and trend following, it is never a bad idea to acquire at least some gold and silver (preferably in physical form) and if possible even a small plot of arable land – and learn how to use it. We’re up for a bumpy ride.